What the AI bubble will leave behind

The software opportunities begin where the capex ends

TL;DR

Bubbles do not just leave assets behind. They leave work.

We think the forgotten story of the telco bubble was the software that made the wreckage usable.

AI’s version is already forming in power, leases, GPU debt, inference bills, and procurement.

Over the last twelve months, the AI bubble question has become a regular part of LP conversations.

At first, it arrived as a perfunctory diligence question near the end of the meeting.

“And what if this is all a bubble?”

It had the energy of a question people mostly ask to prove they asked it. But that is not quite right either, because everyone actually wanted to hear the answer. It was more like checking under the bed for the boogeyman. You do not really believe in the boogeyman. You still check.

Yes. We checked. Twice, obviously.

Then there was the other version, which I liked much more: the LP who came in with an analogy already chambered.

“Isn’t this just fiber, except the fiber depreciates every three years?”

Those are my people. I think that way too. Give me a historical analogy, a broken capital structure, and one weird mismatch in asset duration, and I am happy. The question was never annoying. It was just early.

Now everyone asks it.

And once everyone asks the same question, the question itself stops being the interesting part. The interesting part is what the question assumes.

“What happens if the AI bubble pops?” makes the pop sound like the event. One moment of market-clearing violence. A chart going down. A few spectacular bankruptcies. Some awkward board meetings. The usual cleansing fire.

But bubbles do not just pop.

They leave things behind.

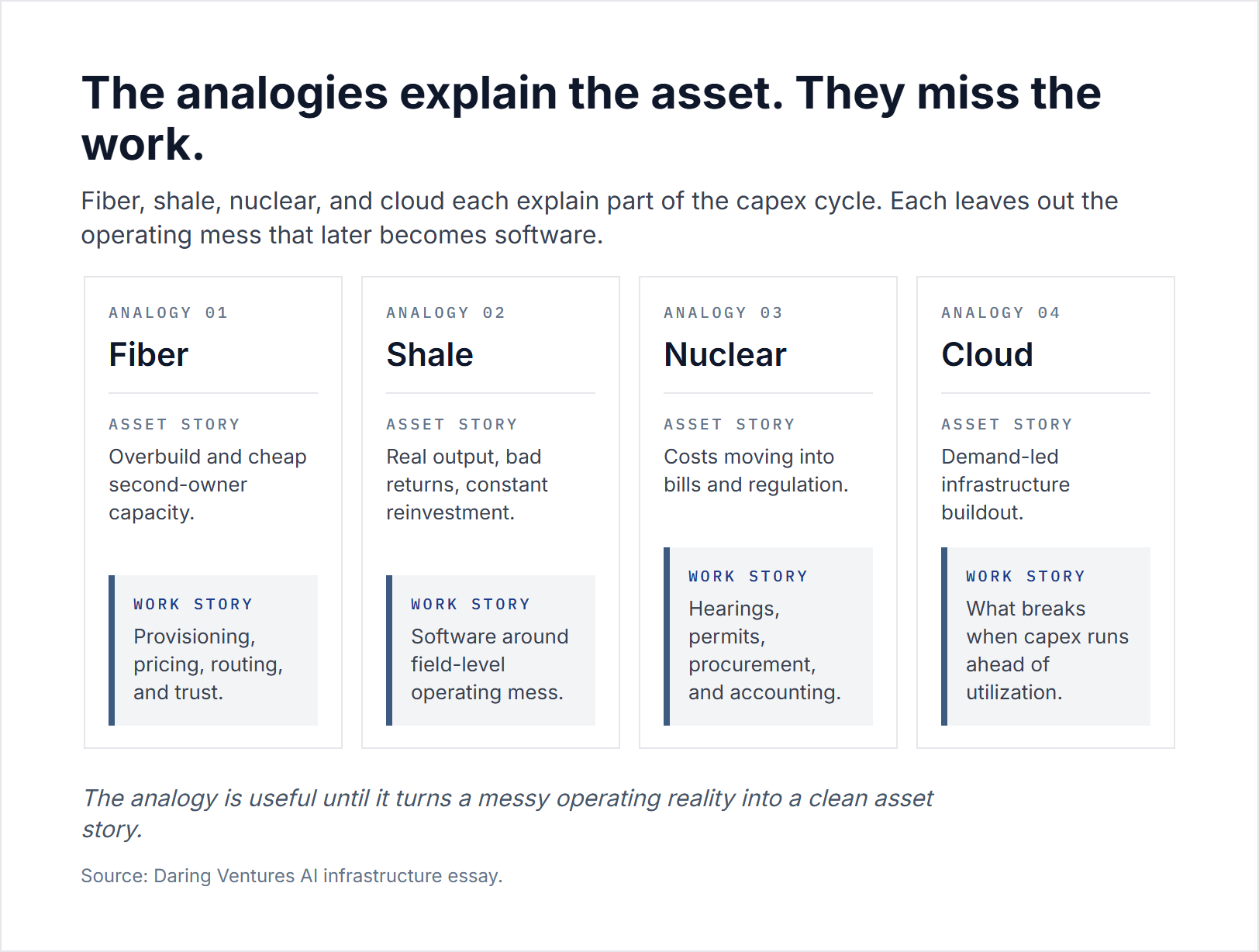

People reach for analogies because there is no clean way to talk about a buildout this large while it is still happening. Fiber. Shale. Railroads. Nuclear. Cloud. Every prior boom gets pulled off the shelf and held up to the light.

The analogies are useful because they turn a live, messy operating reality into a clean historical shape.

Fiber is the comfortable one. The story goes like this: capital overbuilt the network, investors got wrecked, bandwidth got cheap, and society inherited the infrastructure for the next internet.

Perhaps.

Shale is darker. Real output, bad returns, constant reinvestment, asset depletion disguised as growth.

Maybe that too.

Nuclear is less fun to talk about, because the punchline is a power bill. Cost overruns do not vanish. They migrate into rate cases, surcharges, and a thirty-year argument over who should have known better.

Maybe that too.

The problem with all of these analogies is not that they are wrong. It is that they are too clean. They make the cycle sound like a question of asset value. What is the salvage value of the fiber? What is the residual value of the GPU? Who owns the railroad after receivership? Who gets stuck with the plant?

Those are good questions. They are not the only questions.

Buildouts do not just leave assets behind.

They leave a lot of work.

Contracts. Permits. Leases. Tariffs. Billing disputes. Vendor fights. Security gaps.

It becomes consulting. Litigation. Regulation. A private-equity rollup. Which then becomes repeatable workflows, scalable markets, and real software opportunities.

Boom or bust, the rise of process is when software has something to sell because the work it inevitably creates has become somebody’s job.

One power bill, ten workflows

Start with the power bill.

A data center does not just use electricity. It changes who has to reserve capacity, who pays for grid upgrades, who gets priority in an interconnection queue, which costs can be passed through to ratepayers, which projects get delayed, and which regulator has to explain why the same household is paying more for a system it does not think it uses.

That is the part the bubble analogies tend to miss. The asset is easy to point at. The work is not.

In the regional grid market that covers much of the Mid-Atlantic and Midwest, capacity prices for the 2025-26 delivery year cleared at $269.92 per megawatt-day, up from $28.92 the prior year. That is an 833% increase. Data centers accounted for 40% of the December 2025 capacity costs. By 2028, one estimate has the average household in the region paying $70 more per month on its electricity bill.

It’s only one price signal, but it has a cascading effect.

The ratepayer gets a bill. The public utility commission gets a hearing. The state legislature gets a bill. The utility holdco gets a new five-year capital plan. The EPC (energy, procurement, construction) contractor gets a revised schedule. The equipment supplier gets an order book. The tax office gets an abatement fight. The insurer gets a new exposure. The auditor gets a new lease question. The procurement team gets a vendor problem. The associate gets a PDF named final_final_v7.

GE Vernova entered 2026 with 83 gigawatts of equipment under firm order. Siemens Energy is sold out years into the future. Transformer lead times are now measured in quarters, not months. EPC contracts that used to treat equipment as a passthrough now negotiate over turbine slots, transformer reservations, and switchgear queues as first-class economic rights.

Every one of those is a workflow.

The same thing is happening in financing.

A data center lease used to be a real estate document with power density. Now it can be the anchor for a special-purpose vehicle, the collateral behind an investment-grade bond, the proof point for a private-credit fund, the reason a utility files a new rate class, and the invisible bridge between a hyperscaler’s balance sheet and somebody else’s cost of capital.

Meta and Blue Owl’s Louisiana structure has a name now. People call it the Beignet template. Blue Owl owns most of the development entity and bears most of the cost; Meta owns the minority stake and signs the long-term lease back. The debt is rated like high-grade paper but yields like something that knows it is carrying more risk than the rating suggests. Thirty-plus hyperscale campuses are reportedly using or copying versions of the structure.

That is not just a financing innovation. It is a workflow factory.

How do you reconcile a 25-year physical asset against a shorter accounting treatment of the lease? Who carries the renewal risk? Whose insurance covers the residual? Where in the waterfall does the gas supplier sit relative to the preferred equity? What disclosure is required when the same anchor tenant is also a meaningful counterparty elsewhere in the capital stack?

None of these questions sound like software.

That is usually the first clue.

In West Texas, the same thing is happening around behind-the-meter power. The simple thesis is easy to understand: the Permian produces so much associated gas that it can trade at deeply negative prices, and that stranded gas can power colocated compute faster than a utility interconnection. The hard part is everything after the sentence.

Does the project have a named, creditworthy offtake? Does it have an air permit? Does it have turbines secured? Who owns the gas supply? Does the gas contract match the data-center contract? What happens in year fifteen if the gas plant still has a decade of useful life and the compute customer has moved on? Is the water right real? Does air cooling work in a West Texas summer without destroying the power economics? Does the developer have a project, an option, or a press release?

Again, workflows.

Some of them will be absorbed by lawyers. Some by utilities. Some by private-credit analysts. Some by consultants. Some by whichever developer can afford to hire the person who knows the answer. Some by an associate who becomes the only person in the room who understands why the tax abatement, GPU depreciation schedule, gas supply agreement, and tenant guarantee do not quite line up.

A small slice will become software companies.

The companies that get built will not announce themselves as “AI infrastructure software.” They will look, at first, like someone fixing a very specific workflow that suddenly became too expensive to keep fixing by hand.

The asset changes. The cleanup work rhymes.

There is one prior cycle close enough to look at carefully.

Recommended for you

The story people remember

Telecom is the cleanest prior cycle because the public memory of it is so settled.

Everyone knows the headline version. In the late 1990s, capital flooded into fiber. Carriers borrowed too much, built too much, and assumed demand would arrive on schedule. It did not. The bubble broke. Balance sheets collapsed. The physical network survived. Bandwidth got cheap. The next generation of internet companies inherited better infrastructure than the first one had.

That story is true as far as it goes.

It is just not the part that matters most here.

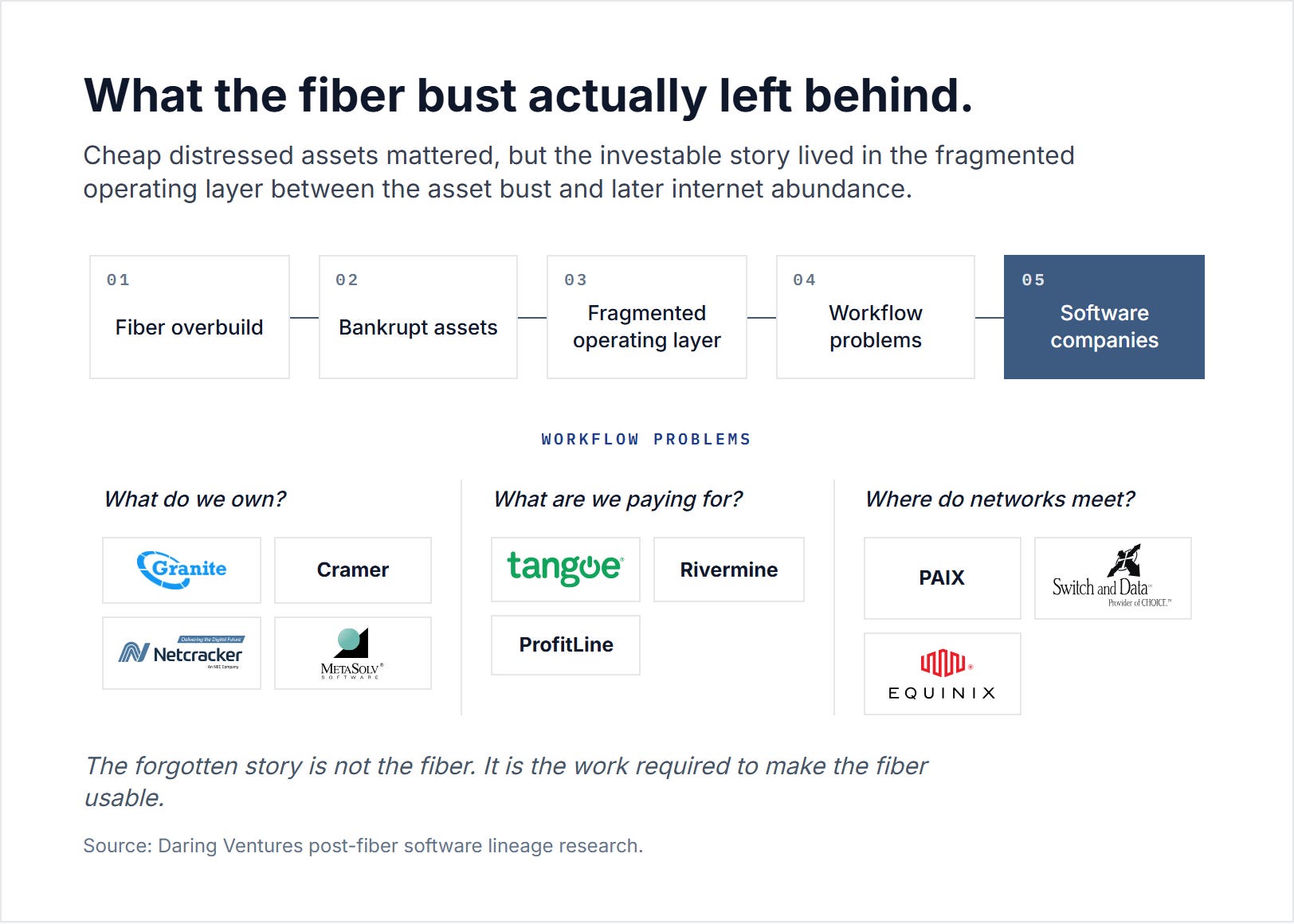

Cheap assets explain why better-capitalized operators could buy distressed networks for pennies on the dollar. They do not explain why the decade after the bust produced a quiet wave of companies most people outside telecom have never heard of. To see those companies, you have to look between the bankrupt asset and the eventual internet abundance.

That is where the work was.

In April 2002, PSINet sold its U.S. national backbone to a four-year-old company called Cogent for $10 million in cash, plus $3 million for the right to do due diligence.

PSINet had spent billions building that backbone. Cogent’s founder Dave Schaeffer had previously run a taxi fleet and a commercial real estate business, and by the late 1990s he had been close enough to dark-fiber economics to know what was about to come out of the Southern District of New York bankruptcy court. Between 1999 and 2002, Cogent did the same trade thirteen times. By 2014, Schaeffer was telling investors Cogent carried roughly a fifth of the world’s internet traffic.

That is the version of the telecom bust I remember from NPR on the way to soccer practice: cheap assets, better operators, second-owner economics.

It’s only half the story though. The neat half. Underneath all the “fiber” were carries that did not know what they owned, enterprises paying invoices for circuits no one used, and a network of operators who had spent enough time inside the pipes to know where the bodies bundles were buried.

The first problem was inventory.

After the bust, the surviving carriers had absorbed fragments of dozens of failed networks. Routes, switches, circuits, leases, customers, billing systems, and physical plant had been stitched together through bankruptcy sales and emergency integrations. Knowing what the carrier owned was no longer a database question. It was an archeological problem.

By 2003, SBC and Telecom Italia were phasing out a Bell System-era network inventory system called TIRKS and replacing it with software from a startup called Granite Systems. Telcordia bought Granite in 2004 for roughly $70 million. Two years later, Amdocs paid $375 million for Cramer Systems, a UK company solving a similar problem. NEC bought NetCracker for around $300 million. Oracle bought MetaSolv for $219 million.

Nobody outside telecom has heard of most of these companies. That is the point. They were not consumer internet stories. They were not Web 2.0. They were software companies built inside the operating mess the bust left behind.

The second problem was the bill.

A 2005 Gartner study found that up to 80% of enterprise telecom invoices contained some kind of mistake. Enterprises were paying for disconnected circuits, abandoned wireless lines, duplicate services, and contracts no one on staff remembered authorizing. The network had become cheap enough to sprawl and complicated enough that no one could audit it by hand.

A category called telecom expense management appeared to clean this up. Tangoe, Rivermine, ProfitLine, Asentinel, and others showed up. Al Subbloie founded Tangoe in Orange, Connecticut in 2000 after a decade inside enterprise telecom procurement (our kind of guy).

He knew where the invoices went to die. Tangoe went public in 2011 and was taken private by Marlin Equity in 2017 for $242.6 million.

The third problem was interconnection.

Once bandwidth was cheap, the scarce thing was no longer just owning fiber. It was being in the right place, with the right networks, under the right operating agreements. The Palo Alto Internet Exchange had been one of the most important neutral peering points in the United States. More than a hundred networks met inside one Bryant Street building.

Metromedia Fiber Network had paid $75 million for it in 1999. When Metromedia filed Chapter 11, Switch and Data bought PAIX out of bankruptcy in 2002 for roughly $40 million. In 2010, Equinix bought Switch and Data for $689 million.

The asset had not changed. The operating context around it had.

These stories are less famous than Cogent because they do not fit the clean bubble narrative. They were not “buy cheap fiber and wait.” They were the systems that made the post-bust network usable.

The bust left behind a fragmented, distressed, mis-billed, mis-provisioned operating layer. Then a generation of companies showed up to fix it, one workflow at a time.

Schaeffer had been close to dark-fiber economics. The Granite engineers had been inside carrier inventory. The Equinix founders had been inside the early internet exchange points. Subbloie had been inside enterprise telecom procurement.

None of them announced themselves as part of the bust.

They announced themselves as people who knew what was broken.

The biggest winners did not look like the asset owners

The next layer was stranger.

By the time Jeff Lawson founded Twilio in March 2008, AT&T had told him three times that integrating telecom into a software product would take two years, cost millions of dollars, and begin with rolling out copper wire.

He had been founding CTO at StubHub. He had built a point-of-sale system at a southern California skate-and-surf retailer. He had been hired by Amazon in late 2004 as one of the first product managers on AWS. He had never worked inside a carrier. He had hit the carrier wall from the outside three times before he started building for it.

That was the workflow.

Twilio’s first product launched November 20, 2008. Lawson rickrolled the TechCrunch editor from a few lines of code. By 2016 the company was public. By fiscal 2025 it generated $5.07 billion in annual revenue on $234 million of pre-IPO venture capital. Twilio’s peak market cap was north of $60 billion.

None of that works in 1998.

The post-bust glut of cheap termination, the dense carrier-neutral interconnects at Equinix, the collapse in wholesale voice and SMS pricing, and the Amazon cloud Lawson had just helped build all had to land first.

Twilio is what you get when the work beneath the telecom boom compounds long enough that the original infrastructure can disappear behind an API.

That same migration happened elsewhere.

Akamai was founded before the bust, but the business only fully made sense once cheap fiber, cheap colocation, and carrier-neutral interconnection made it economical to put servers near users at global scale. Prolexic was built because abundant, always-on connectivity created abundant, always-on attack surfaces. Dyn and ThousandEyes helped enterprises manage the fact that the internet had become mission-critical without becoming internally manageable. Apptio and CloudHealth later did something similar for cloud spend: they helped the enterprise understand a new infrastructure bill that had become too complex to govern by hand.

The important thing is not that these companies were farther away from the physical asset. Distance is the wrong frame.

The important thing is that they sold to a broader buyer.

Granite and Cramer sold to carriers. Tangoe sold to enterprises trying to clean up telecom spend. Akamai, Prolexic, Dyn, and ThousandEyes sold to enterprises whose businesses now depended on the network. Twilio sold to developers who never wanted to talk to a carrier at all. Apptio and CloudHealth sold to CIOs, CFOs, and line-of-business owners trying to govern infrastructure they did not own and could not turn off.

The founder pattern was not identical in the narrow biographical sense. Some had worked inside the buyer. Some had worked inside vendors. Some were academics. Some were developers who kept running into the same wall from the outside.

But they shared something more important than a résumé category.

They were close enough to the workflow to know which abstraction would be trusted.

That is the line between a good analogy and a lazy one. The lesson from telecom is not that every post-bust software company is founded by someone who worked at the original asset owner. That is too narrow, and the history does not support it cleanly. The lesson is that the durable companies were built by people close enough to the operating pain to understand the order in which the mess had to be fixed.

Inventory before automation.

Interconnection before abstraction.

Billing visibility before spend governance.

APIs after the underlying cost structure had collapsed far enough that the API could hide it.

The companies looked obvious only after the layer below them had become stable enough to disappear.

You cannot trade what you cannot provision

There is one piece of the post-bust story that did not produce durable software companies.

In 1999, two industries arrived at the same conclusion at the same time. Bandwidth would soon trade like wheat.

Enron Broadband Services built a trading desk with proprietary network provisioning software and expensive Sun servers. Arbinet ran a NASDAQ-style exchange for international voice minutes and IP capacity, IPO’d in December 2004 at $17.50, and peaked near a $500 million market cap. RateXchange, Band-X, LighTrade, and Global TeleExchange built variations on the same model.

Every one of them failed.

Enron Broadband failed first and most spectacularly: $494 million in losses over the first nine months of 2001. Arbinet held on for six more years before being acquired for parts in 2010.

The founders came from energy trading, commodities finance, and in one case a former military pilot turned deregulation policy director. None of them had run a carrier. None of them had provisioned a circuit. They saw what looked like a commodity and missed that the commodity had not yet become operationally tradable.

The diagnosis was not complicated.

The capacity was not fungible. A circuit between New York and Los Angeles was not interchangeable with one between Chicago and Atlanta. Provisioning was slow enough that the spot-market clock did not work. Asset owners refused to yield pricing control to a third-party exchange. The software required to dynamically measure, route, and trust packets across competing carrier hardware did not exist.

The marketplace required all of that to exist first.

Nobody had built it.

You cannot trade what you cannot provision, measure, route, and trust operationally.

The mistake was not in seeing abundance. The abundance was real. The mistake was in financializing it before the operational middleware was in place.

Bandwidth had its turn in 2000. Compute capacity is having its turn now.

The temptation is older than the asset class. So is the failure.

If someone tells you the opportunity is a GPU marketplace, the first question is not whether GPUs are scarce or abundant. The first question is whether the buyer can trust the capacity, verify the performance, move the workload, understand the security boundary, reconcile the bill, finance the collateral, and get paid when something breaks.

The exchange is the last mile.

The workflow comes first.

Something a little different

The three layers

The telecom cycle did not produce one software market. It produced three.

The first layer sold to the asset operator.

Granite, Cramer, NetCracker, MetaSolv, and parts of the telecom expense management category made the broken operating layer legible to carriers and telecom teams. These companies helped answer basic questions: What do we own? Which physical asset maps to which customer? Which service has been provisioned? Which circuit is still being billed? Which database is wrong?

The exits were real, but the ceiling was set by the buyer base. Carriers were consolidated, indebted, slow to buy, and often still digesting the same wreckage the software was built to manage. Granite sold for roughly $70 million. NetCracker for around $300 million. Cramer for $375 million. MetaSolv for $219 million. Tangoe went private for $242.6 million.

The software mattered. The buyer base was narrow.

The second layer sold to the enterprise that depended on the asset.

Akamai, Prolexic, Dyn, ThousandEyes, and similar companies did not ask enterprises to operate the network. They helped them survive dependence on it. Your application needed to be fast. Your site needed to stay online. Your traffic needed to route correctly. Your security team needed to understand what was happening outside your own walls.

The buyer was no longer the carrier trying to clean up its own plant. The buyer was every enterprise whose revenue, uptime, or customer experience now depended on the network.

The ceiling moved.

Prolexic sold to Akamai for $370 million. Dyn sold to Oracle for more than $600 million. ThousandEyes sold to Cisco for roughly $1 billion. Akamai became the public-company version of the same motion.

The third layer sold to the person who never wanted to think about the infrastructure at all.

Twilio sold to the developer. Apptio sold to the CIO and CFO. CloudHealth sold to the team trying to understand cloud spend. Acme Packet sold into the control plane that made communications infrastructure behave like something software could depend on.

The buyer was no longer “telecom.” The buyer was everyone building on top.

This layer produced the largest outcomes: Acme Packet at $2.1 billion, Apptio at $4.6 billion, Twilio as the public-company version with a peak market cap north of $60 billion.

That is the distinction that matters.

The exit scaled with the breadth of the buyer base, not with the founder’s proximity to the physical asset.

It is easy to tell the story backward and make it sound inevitable. Of course carrier software sold to carriers. Of course enterprise network visibility sold to enterprises. Of course communications APIs sold to developers. But none of this felt obvious from inside the cycle. In 2002, everyone was still staring at bankrupt fiber. In 2004, the interesting company looked like a boring inventory system. In 2008, the interesting company looked like a developer tool for making prank phone calls.

The sequence was not accidental.

The carrier inventory layer had to be partially fixed before enterprises could depend on the network with confidence. The enterprise layer had to mature before developers and CFOs could treat the network as an abstraction. You could not sell the API until the interconnect worked. You could not sell the spend dashboard until the usage existed. You could not make the infrastructure disappear until enough of the work underneath had become stable.

The work moved upward because the layer underneath had become stable enough to vanish.

What is forming now

The AI buildout is producing the same kind of work, but not in the same places.

The lazy version is to map telecom terms directly onto AI terms. Fiber becomes GPUs. Bandwidth becomes tokens. Carriers become neoclouds. Bandwidth exchanges become compute exchanges. Twilio becomes “the Twilio for AI.” This is how bad analogies reproduce. They keep the nouns and miss the mechanism.

The mechanism is not “fiber, but AI.”

The mechanism is: capital commits before the operating layer exists, and then the world has to invent the operating layer.

In AI, the operating layer is forming across several balance sheets at once.

It is forming in power procurement, where utilities are being asked to plan around loads that are large, concentrated, and politically sensitive before end-user AI demand is fully proven.

It is forming in data center finance, where leases, special-purpose vehicles, private credit, and hyperscaler commitments are being used to transform uncertain future compute demand into today’s investment-grade paper.

It is forming in GPU-backed lending, where chips become collateral, collateral values depend on utilization and obsolescence, and lenders need to know whether a three-year-old H100 is money-good in a world where the next generation of silicon has changed the economics.

It is forming in tax abatements, where state and local governments are discovering that the fiscal note on a data center incentive can be off by orders of magnitude once the category becomes real.

It is forming in inference billing, where developers and finance teams are trying to understand a cost structure that behaves nothing like SaaS seat pricing and nothing like cloud storage.

It is forming in security, where model access, data leakage, prompt injection, inference abuse, and usage monitoring are becoming line items in enterprise risk registers.

It is forming in procurement, where the enterprise wants the promise of AI but does not want to underwrite a vendor whose gross margin depends on subsidized compute, related-party cloud commitments, or a model provider’s ability to raise the next round.

Most of this will not become startups.

The first version of every new operating layer is people. People in spreadsheets. People in law firms. People in procurement. People in utility regulatory affairs. People in insurance. People in credit. People in finance teams explaining why the bill moved. People who know the one clause in the one contract that everyone else forgot mattered.

Then, sometimes, it becomes software.

The trick is not to ask, “What is the AI version of Twilio?”

The trick is to ask, “Which workflow is painful enough that the person doing it has become the system of record?”

That was true in telecom. It will be true here.

The AI-inventory company may not call itself inventory. It may start as a way to reconcile GPU commitments against actual available capacity, power constraints, contractual priority, security posture, and depreciation assumptions.

The AI-expense company may not call itself FinOps. It may start as a tool for one engineering team trying to understand why inference costs doubled after a model routing change.

The AI-credit company may not call itself lending infrastructure. It may start as a collateral-monitoring workflow for one lender who realizes that GPU marks, utilization, contract tenor, and hardware generation are all moving at different speeds.

The AI-power company may not call itself energy software. It may start as a queue, permit, turbine-slot, interconnection, and load-forecast reconciliation tool for developers who are trying to figure out which announced campuses are real.

The AI-governance company may not call itself governance. It may start as a way for a CFO to answer a very simple question: who is allowed to spend how much money on which model, against which data, for which business purpose?

The categories will sound obvious later.

They do not sound obvious now because the people doing the work still think of it as work.

What speed changes

There is one important difference between telecom and AI.

In telecom, the work beneath the boom became obvious after the bust. The debris was sitting there. The bankrupt networks had already changed hands. The invoices were wrong. The inventory systems were broken. The interconnection points mattered. A founder could spend three years inside a carrier’s billing system after the crash, leave, and still be early.

The debris was not going anywhere.

This time, the work is forming during the buildout.

The Beignet template appeared in October 2024. Virginia adopted a new electric rate class for large power users in November 2025. GPU-backed lending is already a more-than-$10 billion market with collateral values, covenant tracking, and remarketing workflows still held together by spreadsheets. Behind-the-meter power projects are already being sorted into bankable, option-value, and slideware based on permits, offtake, turbines, water, gas supply, and regulatory exposure.

These are not post-crash artifacts.

They are live workflows hardening in real time.

That changes the identification window.

When the work forms after the bust, the market has time to notice the mess. When it forms during the buildout, the window between “someone should fix this” and “someone is already fixing this” compresses.

That is the only claim worth making. Not that the layer sequence will compress. Not that the exits will look the same. Not that AI has to rhyme cleanly with telecom because history enjoys being useful to investors. It usually does not.

Only this: the first software company built for the work beneath the AI buildout to reach a billion dollars in enterprise value is probably already founded.

The founders are not telling the venture press. They are not saying they are building the software layer of the AI bubble. They are not announcing a thesis about capex cycles, salvage value, or historical analogies.

They think they are fixing a workflow.

The window to find them is shorter than last time.

Were you building or investing in the telecom boom while I was listening to Marketplace in the back seat of my dad’s car? Would love to hear your thoughts!

I absolutely loved this! Thank you so much.