The Midnight Invoice

The Builders Series #002: ServiceTitan

The Builders Series profiles Buyer-Builders in the wild. Start with the thesis.

Every well-capitalized team that tried to disrupt home services looked at the same market and found the same customer.

The homeowner.

They saw consumers who could not find a good plumber, did not know which electrician to trust, and had no easy way to compare quotes. So they built search, discovery, lead-gen, booking, reviews, and marketplaces. The problem was obvious because almost everyone had experienced it. Everyone has needed someone to fix a leak, replace an AC unit, clean a house, or show up when something broke.

ServiceTitan looked at the same market and built for the person on the other side of the door.

Not the homeowner looking for help.

The contractor trying to run the business after the job was done.

That choice was made before the first line of code, before the first investor meeting, before there was a company at all. Ara Mahdessian and Vahe Kuzoyan were not running a competitive analysis of home-services software. They were building something for their fathers.

The customer was never in question because the problem was never abstract.

They grew up watching it.

The Market Was Not the Customer

Home services was never small enough to miss.

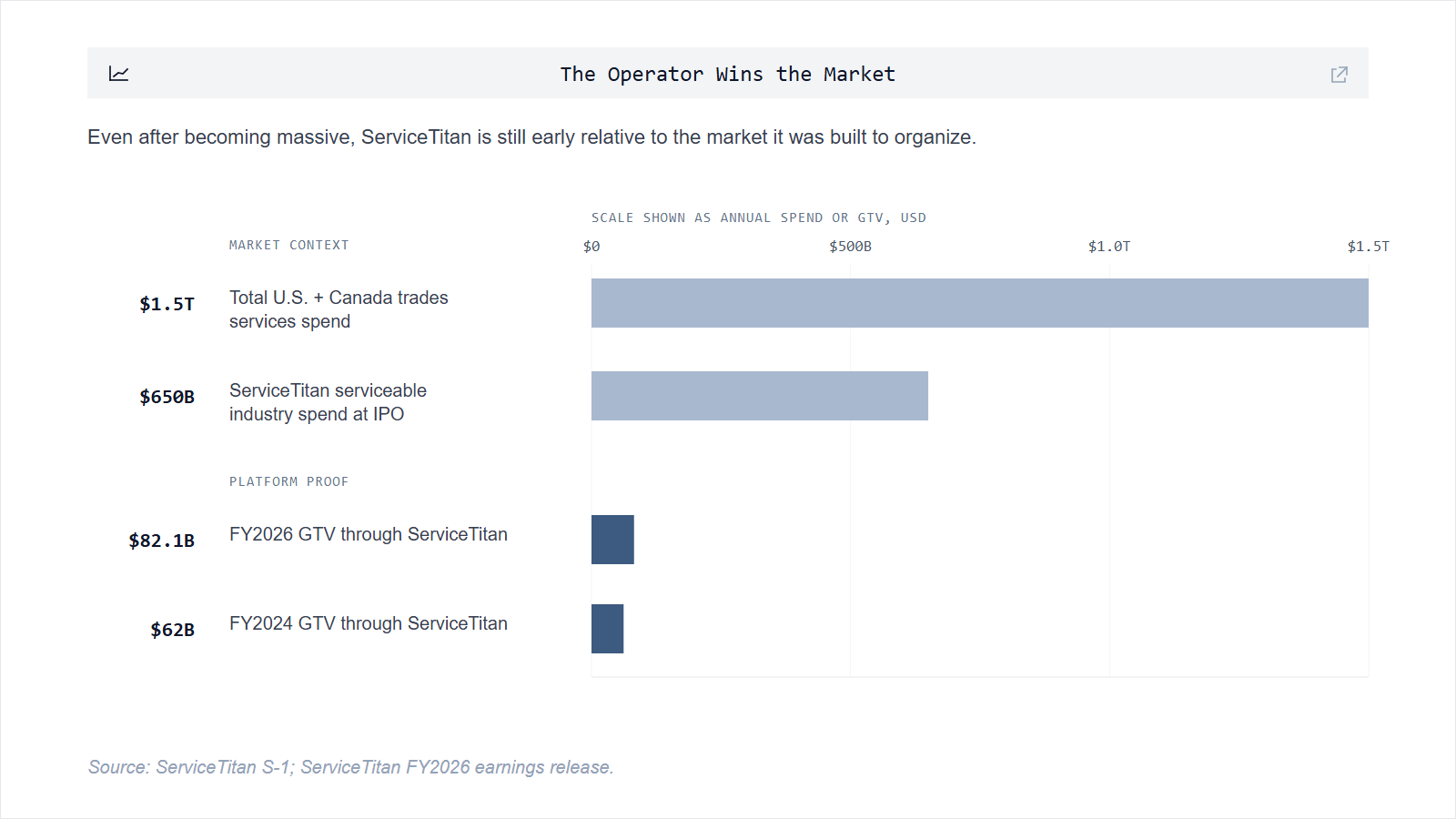

In its S-1, ServiceTitan estimated that end customers in the U.S. and Canada spend roughly $1.5 trillion annually on trades services, with approximately $650 billion inside the trades and end markets ServiceTitan already served at the time of filing.

This was not some hidden niche waiting to be discovered by a clever founder. It was plumbing, HVAC, electrical, roofing, pest control, garage doors, landscaping, and the rest of the work that keeps homes and commercial buildings usable.

The market was visible.

The right customer was not.

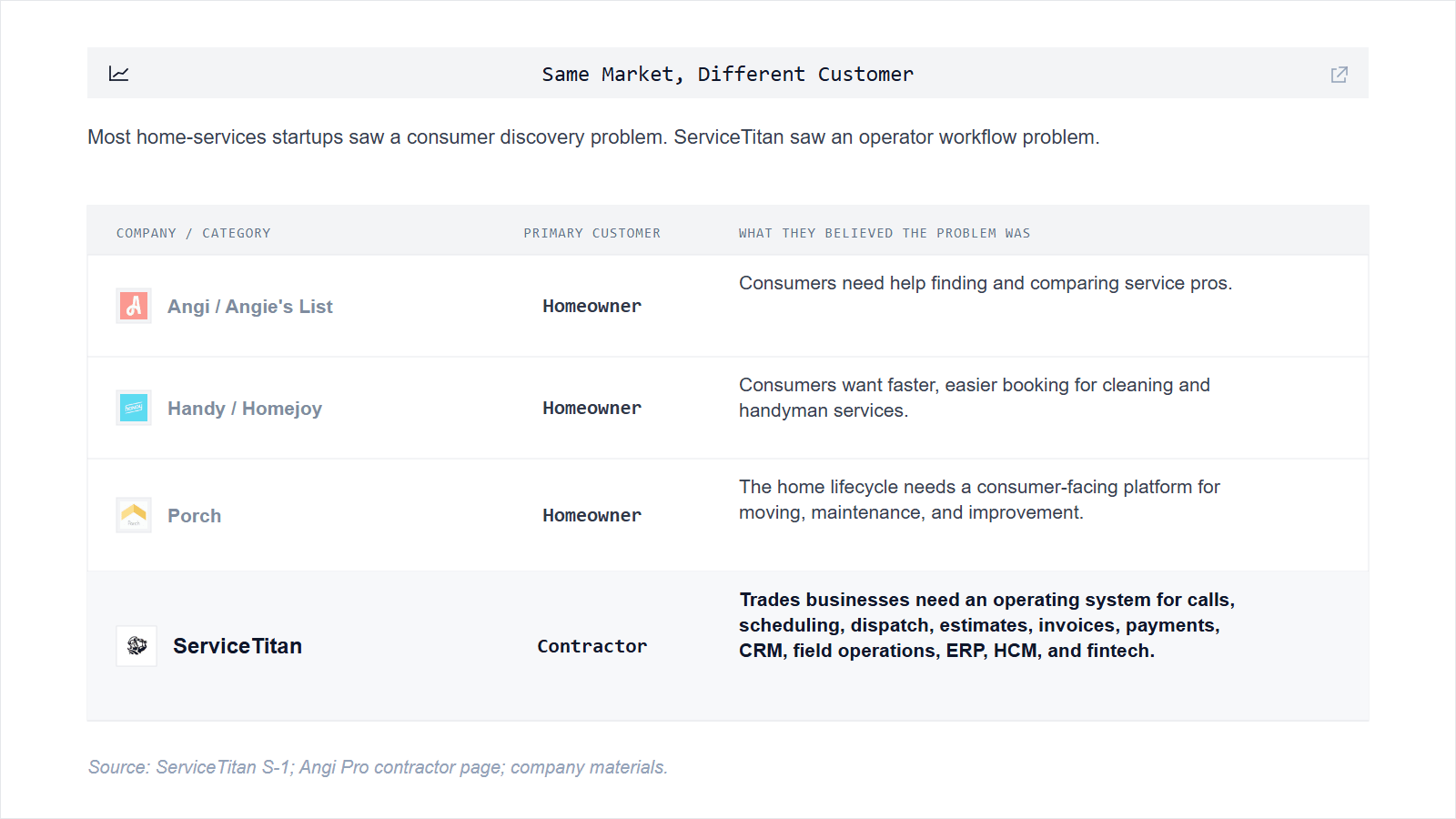

Most companies that attacked the category in the 2010s interpreted the pain from the consumer side. Angi promised contractors access to the “largest homeowner network” and more than 1.5 million monthly opportunities. Handy made it easier for consumers to book home cleaning and handyman services. Porch built around the homeowner lifecycle: buying, moving, maintaining, and improving a home.

They were not wrong that homeowners had a problem.

They were wrong about which problem could become the system of record.

For a homeowner, the drama begins when the sink backs up or the AC dies. For a contractor, the drama began hours earlier and kept going long after the truck pulled away. The phone had to be answered. The call had to be booked. The dispatcher had to know which technician was available, what parts were on the truck, whether the last job was running late, whether the customer was a member, whether financing made sense, whether the quote was profitable, whether the invoice got paid, and whether the owner could make payroll on Friday.

The marketplace version of home services saw the contractor as supply.

The contractor’s son saw the contractor as the customer.

The Business After the Job

Ara and Vahe did not enter home services through a market map.

They entered it through their fathers.

Both were sons of Armenian immigrants in Southern California. Ara’s father ran a residential contracting business. Vahe’s father was a plumber. ServiceTitan’s own company story is direct about the origin: Ara and Vahe originally built ServiceTitan to help their fathers run better contracting businesses.

That detail matters because it changes the shape of the company before the company exists.

The default Silicon Valley interpretation of home services was consumer frustration. Ara and Vahe’s default interpretation was contractor exhaustion.

A marketplace asks:

How do we help the homeowner find someone?

ServiceTitan asked:

Why is the person doing the work still running the business on paper?

That was not positioning. It was inherited context.

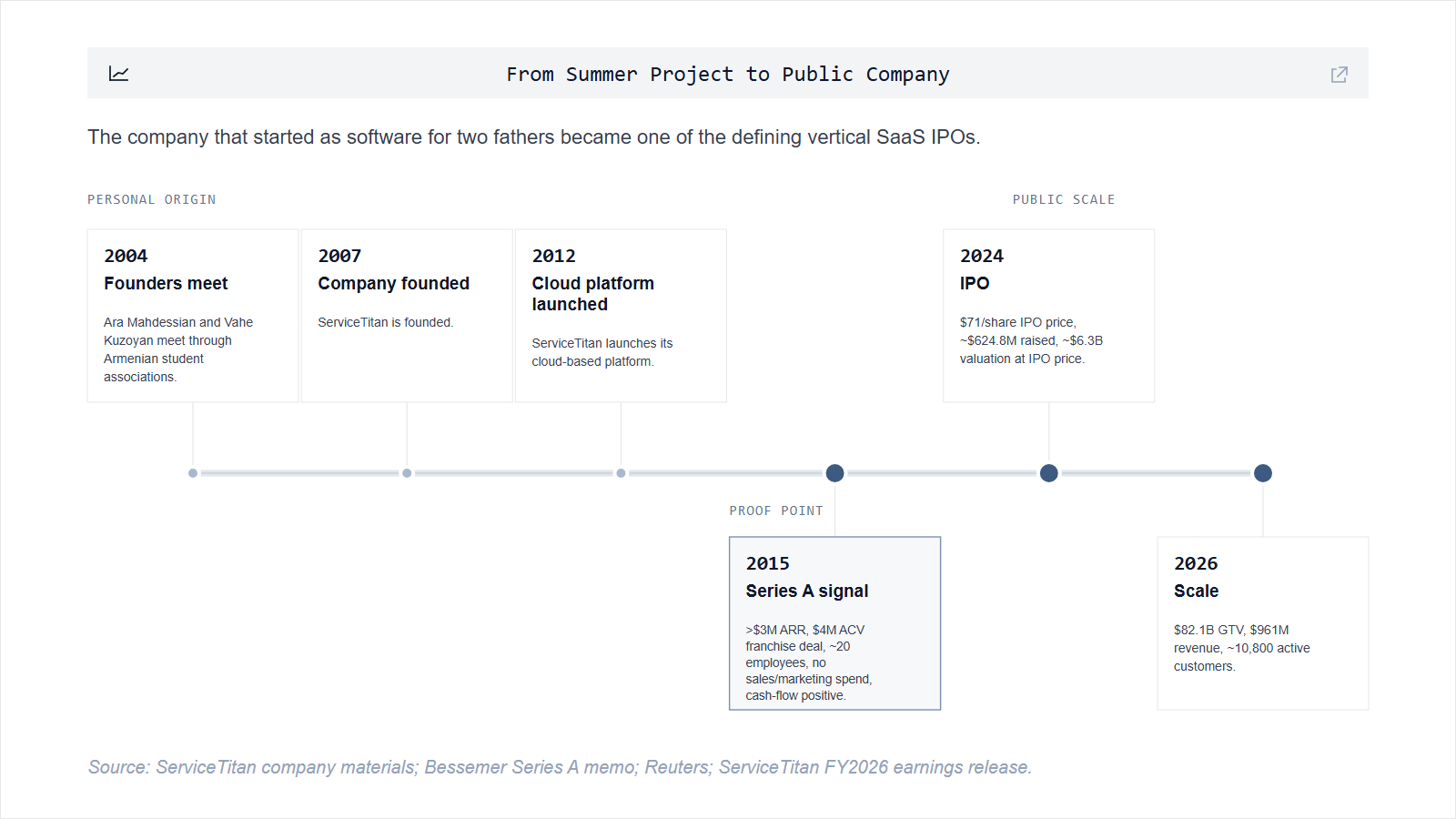

Ara and Vahe met in 2004 through Armenian student associations, began working on software for their family businesses, formally founded ServiceTitan in 2007, and launched the cloud platform in 2012. The early version was not a grand enterprise transformation platform. It was a toolkit for people they knew.

Vahe later described the original motivation simply: he wanted to be useful to his dad. Ara described the early plan as a summer project they could build, hand to their parents, and leave behind before getting jobs at Google or Facebook.

That is not what happened.

Other contractors heard about it. Word spread through the local trades community. The first demand signal did not come from paid acquisition or a polished sales motion. It came from contractors telling other contractors that someone had finally built software that understood how their businesses actually worked.

That is the buyer-builder thesis in its most compressed form:

Insider knowledge does not just determine how you build.

It determines who you build for.

And who you build for determines everything else.

The Search Bar Was a Decoy

The outsider mistake was understandable.

Home services is one of the few categories where almost everyone has felt the consumer pain personally. Everyone has needed a contractor. Everyone has wondered whether a quote was fair. Everyone has heard a story about someone who never showed up.

But personal experience with one side of a transaction can create false intimacy with the whole market.

From the homeowner’s side, the problem looks like discovery.

From the contractor’s side, discovery is just one variable inside a much larger operating machine.

Leads are not useful if the office cannot answer the call, book the appointment, dispatch the right technician, generate a quote, collect payment, and follow up. Demand is not the same as capacity. A booked job is not the same as a profitable job.

This is where the marketplace model quietly loses the plot.

A lead-generation business can help a contractor get more demand. But a contractor drowning in administrative work may not need more demand. He may need a way to stop losing margin in the handoffs.

ServiceTitan built for the handoffs.

By the time it filed to go public, ServiceTitan described its platform as an end-to-end operating system across advertising, scheduling, dispatching, estimates, invoices, payment processing, CRM, field service management, ERP, human capital management, and fintech.

That product surface was not random bloat.

It was the shape of a trades business when viewed from the inside.

Bessemer’s Series A memo described ServiceTitan as sitting “at the core” of daily operations, from inbound call management to mobile dispatching and invoicing to back-office management.

That is the difference between a marketplace and an operating system.

One sends you work.

The other changes how work moves through the company.

The First Moat Was Customer Selection

ServiceTitan did not discover contractors after trying homeowners first.

There was no clever pivot from consumer marketplace to vertical SaaS. The customer was selected before the business model.

That choice shaped everything.

Selling to contractors meant ServiceTitan could become mission-critical. It could touch revenue, scheduling, technician productivity, payments, accounting, customer reviews, marketing attribution, and management visibility. It could grow as the customer grew. It could become harder to rip out with every workflow it absorbed.

Selling to homeowners would have meant fighting for traffic, brand, SEO, conversion, and take rate.

Selling to contractors meant owning the place where revenue actually got created.

By early 2015, before ServiceTitan had become a venture-scale brand, the signs were already there. Bessemer’s memo said the company had grown from roughly $1 million ARR to more than $3 million ARR, landed a $4 million ACV franchise deal, done it with around 20 employees, spent essentially nothing on sales and marketing, and remained cash-flow positive.

Those are not the metrics of a company persuading the market into existence.

They are the metrics of a company the market is pulling out of the founders.

The same memo emphasized that most new customers were coming through referrals and word of mouth. Contractors were not being convinced that ServiceTitan understood them. They were recognizing themselves in the product.

The strongest version of vertical software often starts this way. The wedge does not look like strategy from the outside. It looks too specific, too unglamorous, too close to the ground.

But the specificity is the point.

Ara and Vahe were not trying to “own home services.” They were trying to make their fathers’ businesses easier to run. In doing so, they picked the customer everyone else had reduced to supply.

The Marketplace Tax

The consumer marketplaces created real value.

They aggregated demand, made service providers more discoverable, and gave homeowners more ways to compare options. But their structural incentive was different from ServiceTitan’s.

A marketplace wants more transactions.

A contractor operating system wants healthier contractors.

That difference sounds subtle until you follow the economics.

If a platform monetizes leads, the contractor is often paying for a chance to win work. If a platform runs the contractor’s business, the contractor pays because the system improves booking, dispatch, close rates, collections, reporting, and customer retention.

The first model taxes demand.

The second model expands capacity.

This is why the wrong customer can lead to the wrong product even in the right market.

Homejoy is the extreme version of the marketplace trap. It attacked home cleaning from the consumer side and shut down in 2015 after struggling to raise capital while facing worker-classification lawsuits. The company had already faced growth and revenue challenges, but its CEO said the “deciding factor” was the lawsuits over whether workers should be classified as employees or contractors.

ServiceTitan avoided that entire axis.

It did not need to intermediate labor. It did not need to own consumer demand. It did not need to decide whether the technician was an employee or contractor.

It sold software to the business already responsible for the work.

That was the cleaner entry point and the deeper one.

The outside-in company tries to abstract away the messy operator.

The inside-out company makes the operator more powerful.

The Product Could Only Expand One Way

Once ServiceTitan owned the operating layer, expansion was not a separate act of imagination.

It was the natural consequence of following the workflow.

A job does not stop at dispatch. It turns into a quote, then an invoice, then a payment, then a review, then maybe a membership, then maybe a financing opportunity, then maybe another job.

The technician needs mobile tools.

The CSR needs call tracking.

The owner needs margin visibility.

The office needs accounting.

The larger customer needs multi-location controls.

The consolidator needs standardized processes across acquired shops.

ServiceTitan’s S-1 makes the product logic explicit: CRM, field service management, ERP, HCM, and fintech are the “core centers of gravity” inside a trades business.

The company’s expansion into payments, financing, inventory, accounting, payroll integrations, and AI products followed the actual path of work rather than a generic SaaS land-and-expand diagram.

This is why the numbers began to look less like a niche SMB tool and more like infrastructure.

In the 12 months ended July 31, 2024, ServiceTitan processed $62 billion in gross transaction volume through the platform. In fiscal 2024, its customers completed approximately 109 million jobs through ServiceTitan, and the company had about 8,000 active customers. Its gross dollar retention had been above 95% and net dollar retention above 110% for each of the prior ten fiscal quarters.

By fiscal 2026, the company reported $82.1 billion in GTV, $961 million in revenue, about 10,800 active customers, gross dollar retention above 95%, and net dollar retention above 110%.

Those are not the metrics of a product that helps contractors find jobs.

Those are the metrics of a product that contractors run jobs through.

The Investor Lesson Was Not Just “Vertical SaaS”

It is tempting to reduce ServiceTitan to the obvious category lesson:

Vertical SaaS can produce enormous outcomes in overlooked industries.

That is true, but incomplete.

The deeper lesson is that vertical SaaS only works when the company chooses the right vertical truth.

“Home services” was too broad to be the insight.

“Homeowners need contractors” was too shallow to be the insight.

“Trades businesses are operationally complex, under-softwared revenue machines run by people who have been ignored by modern SaaS” was the insight.

Bessemer got there early from the product and traction. Its memo emphasized that ServiceTitan had strong domain knowledge, that the founders came from plumbing and residential contracting families, and that they had started because they could not find good software for Vahe’s father’s business.

Battery arrived through a broader labor-market lens. Its “blue-collar software” research started with the observation that a large share of the workforce did not sit behind desks and had not received the same software upgrades office workers had. That research led Battery to ServiceTitan.

Different frameworks.

Same company.

The reason is that ServiceTitan sat at the intersection of both truths: a huge underserved labor market and a founding team with lived access to the customer’s operating pain.

The customer selection came first.

The category followed.

The IPO Was the Receipt

ServiceTitan went public on Nasdaq under the ticker TTAN in December 2024.

The company priced its IPO at $71 per share, above the marketed range, raised approximately $624.8 million, and was valued at roughly $6.3 billion at the offering price.

On its first day of trading, the stock rose roughly 42%, with a market capitalization approaching $9 billion around the first-day trading price.

The public-market story was about scale: revenue, GTV, retention, market size, AI, payments, and expansion into more trades.

But the company’s origin still explains the outcome better than the numbers do.

ServiceTitan did not win because it noticed that home services was large.

Plenty of people noticed that.

It won because it understood where the software belonged.

Not in front of the homeowner.

Inside the contractor’s day.

Why We Like This

The software opportunity in overlooked markets is often misdescribed as a digitization problem.

Paper needs to become software.

Calls need to become workflows.

Invoices need to become payments.

Spreadsheets need to become dashboards.

That framing is directionally right and strategically thin.

The real question is:

Digitization for whom?

In home services, the consumer-facing answer produced marketplaces. The contractor-facing answer produced ServiceTitan.

Both looked at the same market.

Only one became the operating system.

This is why buyer-builder fit matters. It is not just a founder credential. It is a market selection mechanism. Outsiders can study a market and still choose the wrong customer because the most visible pain is not always the most valuable pain.

Insiders often begin with the right customer because the pain was never theoretical.

They watched it happen at the kitchen table.

Ara and Vahe did not need to be told that contractors were underserved. They had seen the second shift. They had seen the paper invoices. They had seen the missed dinners. They had seen competent operators lose hours to work that software should have absorbed years earlier.

The insight was not that contractors needed more leads.

The insight was that the contractor was the platform.

That is the pattern we care about in regulated, fragmented, operationally dense markets. The best founders are not always the ones with the cleanest market map. They are the ones who know which user has been forced to carry the system on their back.

In ServiceTitan’s case, that user was not the homeowner searching for help. It was the contractor, after the job was done, still awake with the invoice.

one detail worth pulling out: you can't fake that signal with paid acquisition. if your "vertical SaaS" needs a sales team from day one to find its own customer, something is not right