The AI Margin Paradox

A public market lens on private market investing

tl;dr: AI productivity is real; AI margin expansion is still unproven.

fast framework: Don’t ask whether AI replaces labor. Ask what input stack produces the most output per dollar.

open question: What if the long-term savings never arrive?

Rightsizing. Streamlining. Flattening. Refocusing. Increasing operational efficiency.

The corporate layoff memo has always been an act of linguistic jujitsu: minimize that you’re firing people and maximize the impact of not paying those people anymore.

AI has given the memo a new vocabulary.

We’ve seen a rash of these over the past few months, but there were two that leapt out at me because of the stark contrast between them.

Coinbase & Cloudflare.

Very different companies, very different financial profiles, same family of claim: intelligence tools have changed what it means to run a company. Fewer people, more software, more leverage.

The temptation is to read these as the same story. Or at least as part of the same larger story about AI. I don’t think they are.

Coinbase looks like the old layoff memo in new clothes: a cost correction the company already needed, narrated in the language of AI productivity.

Cloudflare is harder. Cloudflare is making a more ambitious claim: that AI changes the input mix of the company itself. Fewer people in some roles. More compute. More tooling. More infrastructure. More leverage from the people who remain. The abstract AI debate asks whether the technology is good or bad, liberating or destructive, acceleration or doom. The corporate version is more concrete and more useful: does AI actually let a company produce more output per dollar of input?

Not per employee. Per dollar of input.

Because labor does not simply disappear. It gets replaced by something. Tokens. GPUs. Inference. Internal tools. Data pipelines. Evaluation layers. Monitoring. Security review. Vendor lock-in. And the expensive humans still required to make all of it work.

That is the AI margin paradox.

AI may make workers more productive. It probably already does. But productivity is not the same thing as margin expansion. A company that cuts 1,000 employees and spends the savings on compute, chips, tooling, infrastructure, and equity packages for the remaining engineers has not eliminated cost; rather, it has simply changed its shape.

For now at least, it appears the arrival of a free lunch has been greatly exaggerated.

Jack the narrative

In February, Jack Dorsey announced that Block would cut more than 4,000 jobs, nearly half the company, as part of an AI-driven overhaul. Dorsey’s line was the kind of thing public markets were ready to hear:

“Intelligence tools have changed what it means to build and run a company.”

That is a beautiful sentence if you are holding a bloated cost structure and need to make it sound like a strategy. In the past, we might have called this cost control. In the language of the new world, this is AI-driven innovation.

It moves the cut from the past tense to the future tense. The company is not correcting something. It is adapting to something.

Do not let a great media narrative go to waste, right?

Want to read 6,000 words on AI doomerism? Yeah you do.

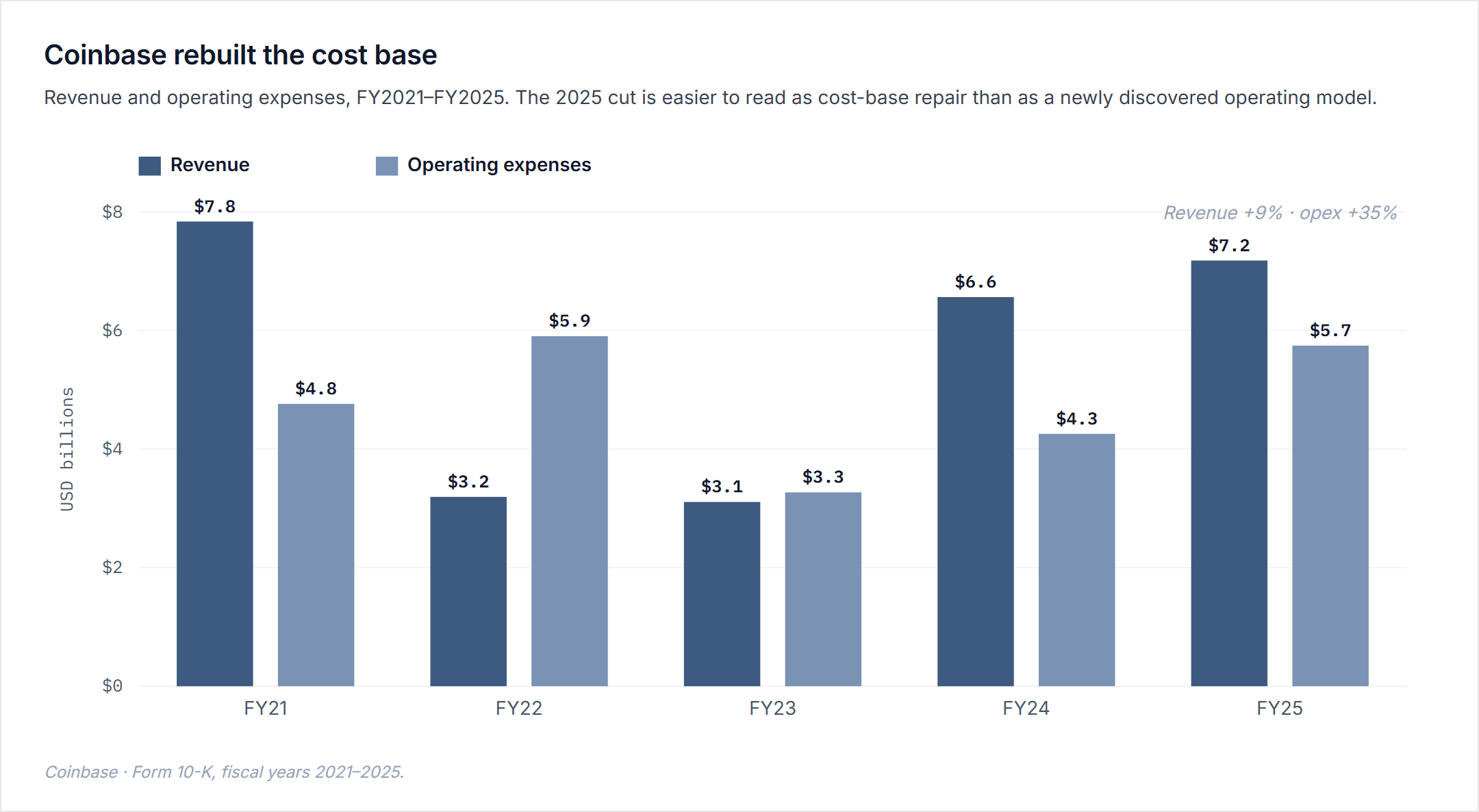

Coinbase: the admission

Coinbase is the cleaner version of that story.

In May, Coinbase said it would cut about 700 jobs, roughly 14% of its workforce, as it trimmed costs amid crypto-market volatility and repositioned for the AI era. The restructuring would cost $50 million to $60 million, and Brian Armstrong cited AI tools allowing smaller teams to ship code and automate work.

That sounds like the future.

The filings sound like the past.

Coinbase had already lived through the first version of this cycle. It hired into the 2021 crypto boom, cut during the 2022–2023 downturn, then re-expanded. There was no AI productivity restructuring hiding in the 10-K. There was no “we have discovered a new operating model.”

There was hiring.

The income statement had already made the next move obvious. Revenue grew, but operating expenses grew faster. The company had restructured, told the market it had learned discipline, and then quietly rebuilt the cost base. The AI letter gave it a better way to reverse itself.

This is cost correction.

And it is not necessarily bad. Sometimes the company really did need to confess. Sometimes the right move is to cut the thing you should not have built back up.

The market can understand that trade because it is not really about AI. It is about taking costs out of a volatile, transaction-sensitive business and giving investors a cleaner path to profitability.

The AI framing matters because it makes the cut feel offensive rather than defensive.

Without AI, Coinbase is cutting because crypto volumes are volatile and management over-hired again. With AI, Coinbase is becoming lean, fast, and AI-native.

Same action. Better tense.

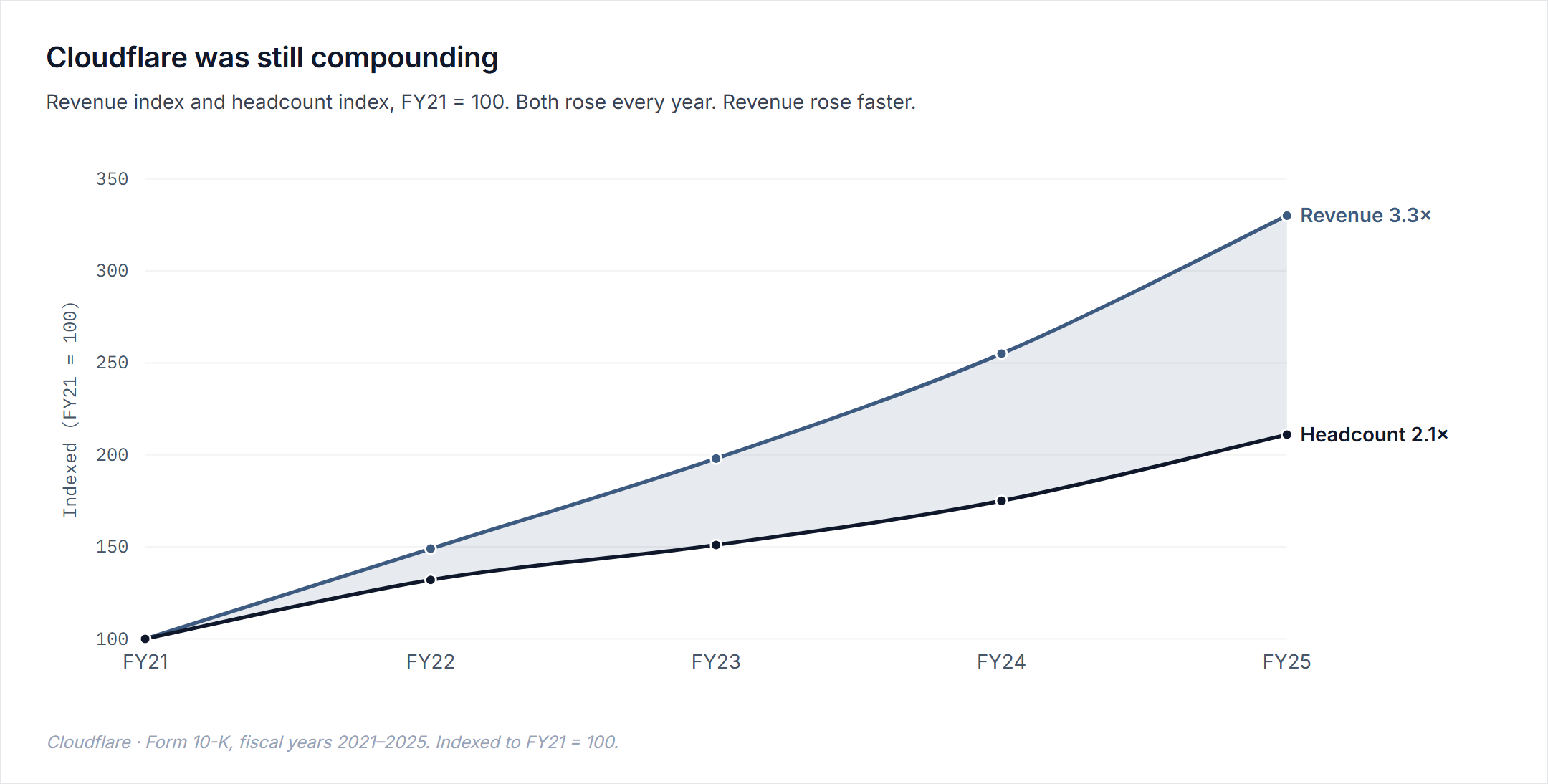

Cloudflare: the investment

Cloudflare is harder to understand, and I think that is the point.

In May, Cloudflare said it would cut about 20% of its workforce, more than 1,100 employees, after internal AI use increased more than sixfold in three months. The memo was not written like a cost-cutting memo. It was written like an operating-system migration.

Cloudflare said the cuts were not about individual performance or short-term cost pressure. The company said it was reimagining internal processes, teams, and roles for the agentic AI era. Matthew Prince later clarified that very few engineers or customer-facing salespeople were affected, and that Cloudflare would continue hiring in those roles.

That makes Cloudflare different from Coinbase.

Coinbase is shrinking the human-cost bucket. Cloudflare is changing the mix of inputs. It is not just saying fewer people. It is saying fewer of some kinds of people, more AI tooling, more infrastructure, more internal agent usage, more product surface around inference, and more operating leverage through a different company architecture.

Cloudflare’s five-year picture looks nothing like Coinbase’s. Revenue compounded more than 3x from 2021 to 2025. Headcount rose every year and more than doubled over the same period. Cash from operations improved meaningfully. Revenue per employee rose. Cloudflare looked like a company expanding the market, not one cleaning up a prior hiring mistake.

And yet 2025 exposed the tension.

Operating margin had improved for years, then stalled. Gross margin compressed. Capex jumped. SBC remained large. Cloudflare’s AI references in the 2025 10-K were about product and network capacity, not internal headcount transformation. Then, weeks later, the company described a 20% cut as part of an agentic AI-first operating model.

The market responded with a 20% cut to its market cap.

A Startup Claim With a Public P&L

The Cloudflare selloff is not necessarily a verdict on Cloudflare’s strategy.

It is what happens when a startup claim shows up inside a public company.

Early-stage founders make this kind of claim every week.

We do not need ten implementation managers because agents handle onboarding. We do not need a large support team because the product resolves tickets itself. We do not need a services-heavy deployment model because AI turns messy customer inputs into structured workflows. We do not need the old headcount shape because the company is built around a different operating system.

Maybe.

But that claim is not proven by saying “AI.” It is proven only when the product ships faster, customers get served better, gross margins hold, and the compute bill does not eat the savings.

That is why Cloudflare is interesting. It is not just a public-company layoff story. It is an AI-startup operating claim appearing on a public-company income statement.

And that’s why as an early-stage vertical AI investor, I’m paying attention.

Every AI-native startup is making some version of Cloudflare’s claim. Cloudflare is just large enough that the claim has to touch the P&L.

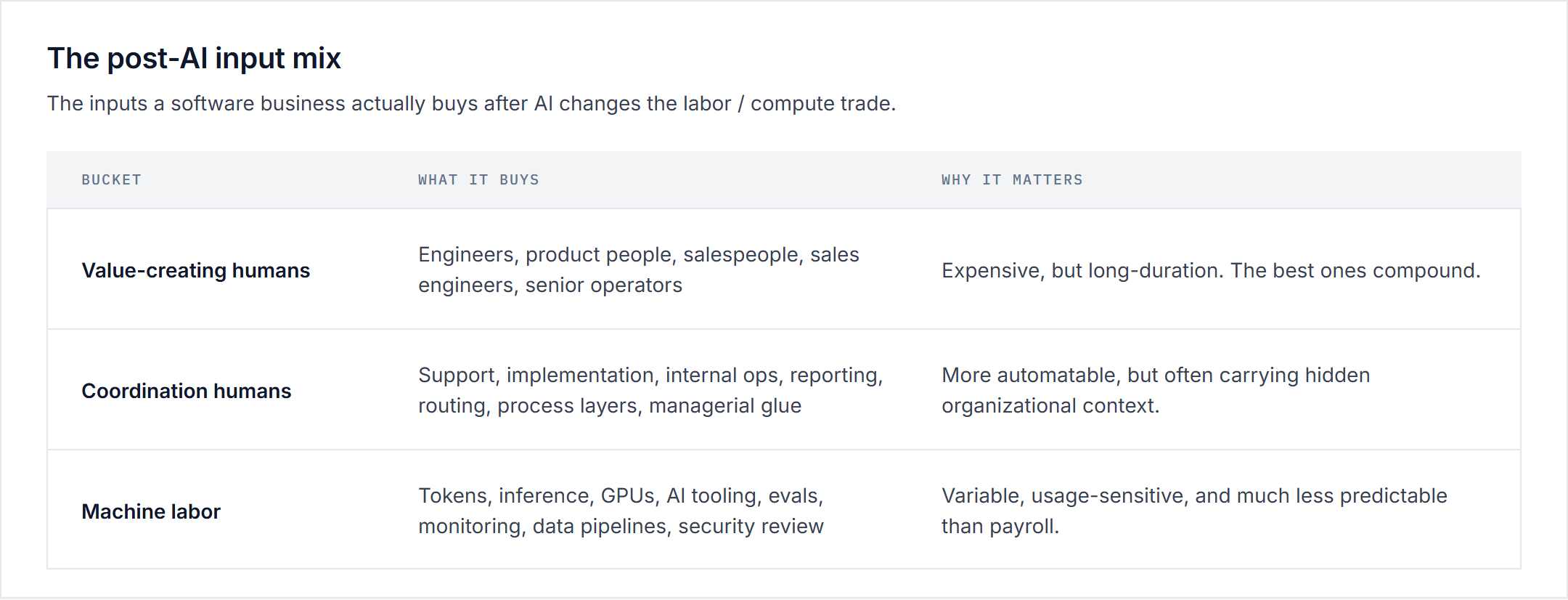

AI vs. Margins

The AI margin story is usually told as if costs associated with labor simply disappears. Perhaps there are very short term dislocations, but the financials show how costs shift. The post-AI cost base has three buckets:

AI does not simply reduce the first bucket. It expands the other two. Sometimes that is a great trade. Sometimes it is a terrible trade. Most of the time, right now, nobody knows.

A software company can announce that AI tools let one engineer do the work of five. Great. What does that mean for Codex usage? Claude Code? Internal tooling? Model-router spend? Fine-tuning? Inference? Evaluation? Security review? Monitoring? Data pipelines? Prompt caching? The GPU bill? The vendor lock-in? The human review layer that appears after the agent fails in production?

Payroll is boring, which is another way of saying it is predictable. Compute is not.

A salary is a number you know in November when you set the budget. Compute is a monthly surprise party hosted by your most enthusiastic users, most ambitious engineers, and whichever lab dropped the “most capable model ever” that billing cycle.

This is where the public market data is starting to get interesting.

The Information’s recent survey of public tech earnings calls showed the spread. Spotify said headcount was down slightly, but compute per employee was rising, including spend on Claude Code and Codex. Shopify’s AI assistant Sidekick was popular with merchants, but merchant usage raised LLM costs enough to partly offset customer-support savings.

When AI works, people use it more.

When people use it more, the bill goes up.

The thing replacing support cost also creates inference cost. The thing helping engineers ship faster also creates tool spend. The thing letting the company slow headcount growth also creates an entirely new class of variable expense.

The labor savings are recognized this quarter. The compute bill arrives later.

Why buyer-builders matter

Every AI deal at pre-seed is making a small Cloudflare-shaped claim: the company can use AI to serve customers with a different mix of humans and machines.

The risk is that the founder spends compute on a workflow that does not actually matter.

That is where the buyer-builder thesis becomes relevant.

We think the future of software will be written by former customers. Read the thesis here:

Not because buyer-builders magically solve the compute-cost problem. They don’t.

They solve a different problem: they reduce the odds that you spend compute on the wrong workflow.

A generic AI founder starts with the tool. A buyer-builder starts with the broken process.

That difference matters more now, not less.

If compute is cheap and predictable, you can afford to spray automation at vague pain. But if compute is variable, usage-sensitive, and capable of eating the margin you thought you were creating, then workflow precision becomes more valuable.

You need to know exactly where the work breaks, exactly who pays for the fix, and exactly how much human cost, delay, error, or risk the software is replacing.

The buyer-builder has already lived that.

They know which task is annoying but worthless, and which task is ugly but budgeted. They know which workflow looks small from the outside but controls the whole day. They know where the customer will tolerate imperfection and where the customer will not. They know which “AI automation” will actually save money and which one will just create a new review queue.

That is the private-market version of the Cloudflare question.

Cloudflare is asking investors to believe that a new mix of humans, agents, and infrastructure will make the company more efficient. AI-native startups are asking customers to believe the same thing, one workflow at a time.

The safest version of that claim does not start with “AI lets us use fewer people.”

It starts with:

I know this workflow well enough to know where AI is worth paying for.

That is why buyer-builders matter. The context they bring through direct industry knowledge makes the value of AI-augmented workflows more legible.

That is better for investors, sure.

It is also much better for acquiring customers.

Public companies are large enough to show the trade. Startups make the same trade before the numbers are visible.

At pre-seed, the AI margin story is usually still a sentence in a deck. The founder says the company will need fewer people because agents will do the work. Maybe that is true. But somewhere underneath that sentence is an input mix: model calls, evals, monitoring, review, edge cases, and the cost of making the system reliable enough to charge for.

The open question is which one compounds faster: AI productivity or AI cost.

That is not a public-market question or a private-market question.

It is the AI company-building question.

Outside of tech businesses, it seems margin is where the AI gains are

https://millennialmasters.net/p/ai-business-model-margin

the buyer-builder thesis closing it out is the part that matters at pre-seed. knowing exactly which workflow is worth the compute spend is the moat. saved this one for the team. thank you