Owning Ops

Our lens on investing in Vertical AI for Services SMBs

At Daring Ventures, we spend a lot of our time looking at software companies serving SMB operators in regulated, physical, and services-heavy industries.

These are the businesses that run on materials, labor, scheduling, invoices, dispatch, compliance, and physical work. They have been promised a software revolution every five years and have rarely received one that survived contact with their day.

We think the next version is finally arriving, and that the right way to invest in it is meaningfully different from what venture capital tried to do in these markets last decade.

Our view here comes up in LP conversations so much that we decided to share how we think about the category.

The marketplace mistake

The 2010s playbook for these industries was the demand-side marketplace. Companies aggregated fragmented supply, connected it to consumers, and took a percentage of the transaction. Some of those companies worked, and most of the ones we care about did not.

The structural problem has two parts. The first is disintermediation. The value created by introducing a homeowner to a roofer, or a diner to a restaurant, or a shipper to a carrier, dissipates almost immediately after the introduction. Your roof is not going anywhere, your favorite restaurant is around the corner, and your trucking carrier already has your number. The marketplace eats the acquisition cost on the first transaction and rarely gets a second crack at the customer. The take rate gets crushed by direct repeat business that the platform paid to manufacture.

The second is geography. These are physically constrained markets. You cannot import a roofer from another town, and you cannot deliver a meal from across the country. The marketplace cannot use scale to compress unit economics, because the economics are determined by the local supply and the local demand, both of which the platform has to keep buying.

Marketplace vs. Operations

There is also a funnel problem inside many of these businesses. Residential services contractors, for instance, spend somewhere around 10 percent of revenue acquiring customers and present the estimate at the kitchen table only after the entire acquisition cost has already been paid, which is why the homeowner experience can feel like a gentle hostage negotiation. We are not interested in fixing that funnel. The contractor’s funnel is the contractor’s problem. The opportunity for us as investors is not in front of the funnel. It is underneath it.

An ops-focused software wedge.

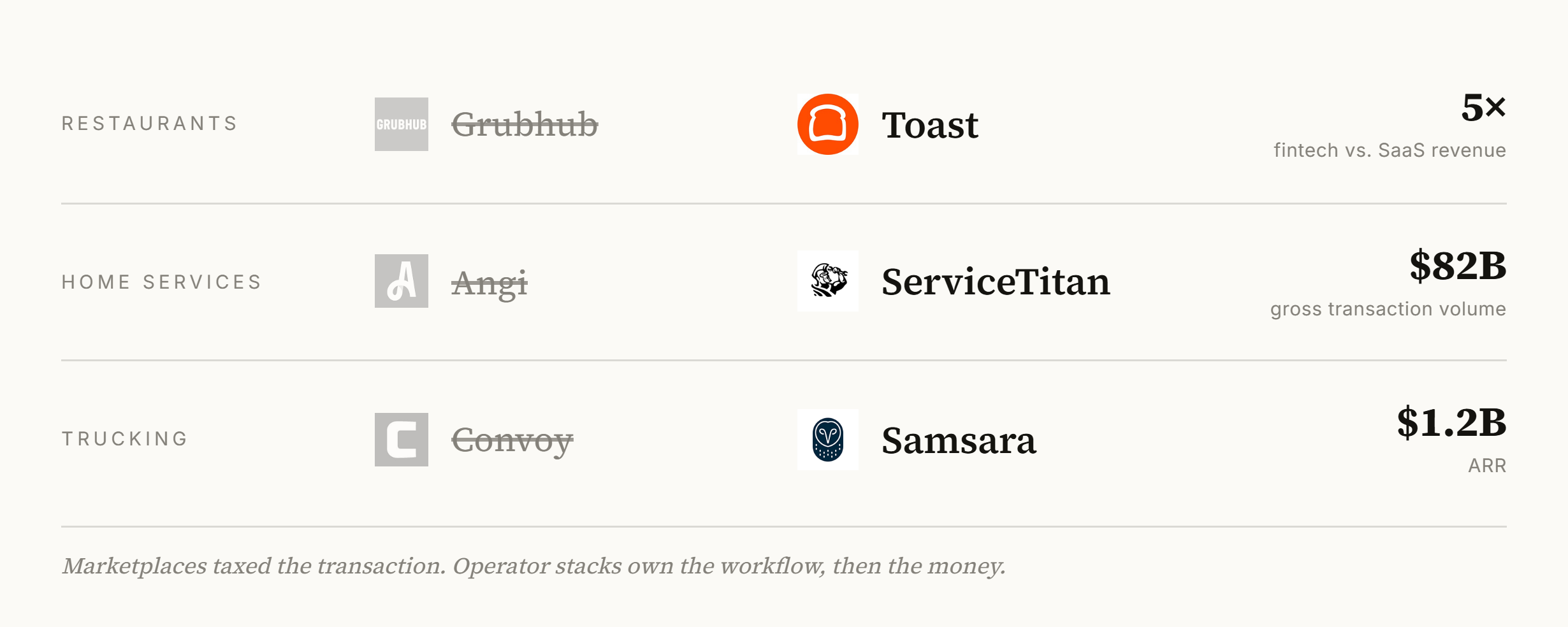

What we have actually seen work in these categories is a different shape. The company starts as software, captures the operator’s daily workflow, and then expands into the financial layer because the operator’s binding constraint is almost always economic rather than informational. Toast generated approximately $5 billion of fintech revenue in its most recent fiscal year against $936 million of subscription revenue. Shopify reported 76 percent of its revenue from Merchant Solutions, with $248 billion of GMV flowing through Shopify Payments. ServiceTitan reported approximately $82 billion of gross transaction volume across roughly 10,800 active customers, and integrated Affirm into the technician workflow last year so financing happens at the moment of estimate.

We look for a few specific things inside that pattern.

The first is buyer-builders. The founders most likely to identify the right workflow are the ones who already lived inside it, and whose first ten customers are reachable through a phone tree rather than a paid funnel. We would rather back a founder who spent a decade inside the industry being served than one who spent a decade building software somewhere else and is now shopping for a vertical to apply it to.

The second is what we call single-player utility. The product has to be useful to the first customer the moment they turn it on, with no network effect required. If the company has a cold-start problem, the company has the wrong product. The right shape is software that solves a specific operator’s pain on day one and incidentally creates the data layer that lets later products attach to the same surface.

The third is a path to a B2B marketplace through the supplier side rather than the consumer side. Suppliers in these categories are not geographically locked the way contractors are. A regional aluminum supplier sells across multiple states, and a restaurant equipment distributor serves dozens of chains. Going to the supplier means going to the participant in the chain with budget, with pain, and without the geographic lock that kills the demand-side version.

Read our investment thesis

Why now

We have been hearing some version of “AI changes vertical software” for two years, and most of the framings collapse on contact with the actual ground reality. These are the primary drivers we’ve identified.

AI is genuinely good at the repetitive, awkwardly shaped tasks that have historically been too messy to digitize at a reasonable cost. AI can reconcile six thousand SKUs across paper catalogs and emailed PDFs without a custom integration. It can extract line items from a hand-drawn site sketch that a contractor walked in with. It can read a supplier’s tier-pricing table directly into an estimate without anyone retyping anything in between. None of this is glamorous AI, and all of it used to require a custom build on every customer.

Voice and vision are now usable input modalities in the field. The technician can describe a job out loud while walking the property and get a structured estimate back. The dispatcher can take a picture of the work site and have the system read the equipment list off the photograph. These input modalities capture data that previously did not exist, because the operator was never going to type it into a form on a phone at the end of a fourteen-hour day.

AI lets the software adapt to the operator instead of forcing the operator to adapt to the software. Most legacy vertical SaaS in these industries was built around a data model designed for someone in a corporate office, and most of the operators we are trying to serve assume CRUD describes CRM because every CRM they have ever used was, in fact, terrible. Software that meets the operator in their own vocabulary, with their own workflow, on their own schedule, was not really possible before. It is now.

This is the corner of vertical software we expect to spend most of the next decade in. It is where the actual money moves through real-world operations and services, and the founders who understand the chain are the ones we want to be in business with. If you or someone you know is building in this space, we’d love to hear from you.

great thesis, we'll make sure to translate this to founders in our briefings. the buyer-builder pattern is the part most need to hear

Interesting read, thanks for sharing.